Premium Services

Featured Results

Your Recent Searches

No Recent Searches Found

Did you mean:

But let's try once more with some tweaks

- Make sure all words are spelled correctly

- Try using fewer words

- Try using more general keywords

- Try different keywords or spellings

Sorry, We couldn't find what you are looking for. It could be because of many reasons.

But let's try once more with some tweaks

- Make sure all words are spelled correctly

- Try using fewer words

- Try using more general keywords

- Try different keywords or spellings

Hi, anything I can help you with?

Financial Education Center

Get answers to common financial questions and dive deeper into topics like auto and student loans, mortgages, personal finances, and more.

Gen Z Financial Habits

Gen Z is taking charge of and is more confident with their finances than we think. See how similar you are to Gen Z with your financial habits.

Fraud Articles

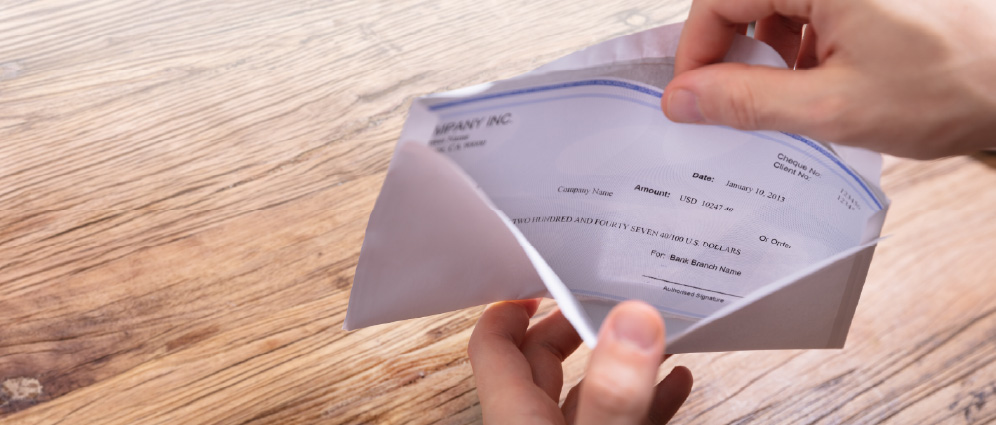

How To Identify and Report Check Fraud

You may not write many checks anymore, but check fraud is still rampant. Keep your finances in check by learning how to identify and report check fraud.

How To Protect Your Bank Account From Hackers

Managing your bank accounts has never been easier, but cybercrimes are becoming an increasing threat. Protect your accounts from fraud with tips from DCU.

Common Two-Factor Authentication (2FA) Scams and How to Avoid Them

Two-factor authentication has become a common and effective form of online security, but what happens when you fall victim to a 2FA scam? Learn more from DCU.

Common Artificial Intelligence (AI) Scams and How to Avoid Them

Worried about AI scams? Protect your personal information and hard-earned money with information, advice and strategies from DCU.

%20Fraud%20Examples%20banner.jpg)

Common Account Takeover (ATO) Fraud Examples

The threat of account takeover (ATO) fraud is growing. A not-for-profit credit union, DCU shares how dangerous these attacks are and how to avoid them.

A Comprehensive Guide to Check Fraud Prevention

Learn about several common check fraud schemes and how to prevent them, along with how to spot check fraud, and the steps for victims to take after detection.

What Is Account Takeover (ATO) Fraud and How To Prevent It

DCU shares what account takeover (ATO) fraud is, how it can negatively impact you and your finances, and what can be done to prevent it before it happens.

How to Protect Yourself From Identity Theft

Learn about the dangers and warning signs of identity theft, as well as the preventative measures you can take to deter it from the experts at DCU.

How to Identify Signs of Elder Financial Abuse

If you are concerned a relative may be the victim of elder financial abuse, check out this guide from DCU. Learn the signs and what you can do to help.

What is Social Engineering and How Do I Protect Myself From It?

Social engineering is how hackers manipulate people into giving up private data. Find out more about what it is and how to protect yourself from it.

Your Complete Guide to Impersonation Scams, and How to Avoid Them

Impersonation scams are a constant threat to our financial well-being. Follow this guide from DCU to learn how to avoid becoming a victim to a variety of scams.

Phishing and Pharming Scams: What to Watch For

Phishing and pharming are two common types of scams, intended to manipulate individuals into providing confidential information for fraudulent purposes. Here’s some tips on how to spot them.

Why You Need to Keep Your Devices and Web Browsers Up to Date

Keeping your devices and web browsers updated is essential to protecting you against fraudulent activity and theft of sensitive financial information.

Fraud Videos

Fraud Podcasts

Podcasts provided courtesy of ![]()

Auto Loans

How to Save for a Down Payment on a Car

If you are shopping for a new or used vehicle but struggling to put together a suitable down payment to get the car you want, DCU has tips on how to save.

What is a Joint Loan?

Read as DCU explains what joint loans are, how they work, plus how they differ from individual loans and co-sign loans, and more.

How to Sell A Car with A Loan

Looking to buy a new or used vehicle but stuck with negative equity? Explore DCU’s guide which details how to sell a car you have a loan on.

How to Refinance Your Car Loan

Want a better interest rate, lower payment or both on your auto loan? With this guide from DCU, learn how to refinance a car loan, which could help you save.

Your Guide To Auto Loan Refinance

Find out the right time for a refinance auto loan. Discover the value of refinancing your car and how to get the lowest auto refinance rates.

What to Look for in an Auto Loan Refinance

If you’re considering refinancing an auto loan to save money, it’s important to evaluate the terms and make sure you’re getting the best deal. Here are 3 things to look for when comparing auto refinance options.

Be Prepared Before Buying a Car

Whether you’re shopping new or used, get tips from DCU on the car-buying process. Learn how to get a good deal and be happy with your car loan.

When Is the Best Time to Buy a Car?

Learn about the best time of the year, month, and week to buy a car with tips from DCU. You could save money on your next auto purchase.

The Perks of Financing Before Car Shopping

If you're planning a vehicle purchase, you probably have an idea of your budget. But have you considered how much that purchase will end up costing over time? Getting approved for auto financing before you hit the dealership can help you get the best deal.

Love Your Car But Not Your Loan?

If you’re unhappy with your car loan and wondering if there’s potential to lower your monthly loan payment, you might want to consider refinancing. This article explains how refinancing works and when it makes sense.

Where Is the Best Place to Get a Car Loan?

If you are in the market for a new or used car, you have options for financing. Discover which institution types might have an option that suits your needs.

How Do Car Rebates and Dealer Incentives Work?

Many car dealers offer enticing incentives on new cars, including 0% interest, rebates, and bonus cash. DCU explains how rebates and deals really work.

What Are Green Auto Loans?

Explore the benefits of green auto loans, the best loans for electric car financing, and how DCU can help you purchase your dream clean-energy car.

How Does Your Credit Score Affect Buying a Car?

Wondering “how does your credit score affect buying a car?” From purchase power to how your score is impacted, this article from DCU has the details.

3 Signs You Should Refinance Your Car

Refinancing your auto loan can add up to big savings, but only if the time is right. Here are the three signs you should look for when considering an auto loan refinance.

Credit Cards

Benefits of DCU’s Visa® Signature Cash Rewards Card

Learn about the advantages of DCU's new Visa Signature Cash Rewards Credit card, replacing the Platinum Rewards card for both future and current cardholders.

Understanding Your Credit Score and How to Improve It

Learn how to improve your credit score. It might be simpler than you think to understand, improve and maintain your credit, especially with the help of DCU!

How to Manage Credit Card Debt

Explore tips for paying off credit card debt and staying debt-free. Learn more about how DCU, a not-for-profit credit union, can help you thrive financially!

Is a Credit Union Credit Card Worth It?

Wondering about the differences between credit union credit cards vs bank credit cards? Read about the many benefits of credit union credit cards.

Tips for Holiday Credit Card Spending

Holidays are a time for celebration, giving, and inevitably—spending. DCU offers tips for using credit cards wisely during the holiday season

Store Cards: Are They Worth It?

It pays to evaluate credit card offers carefully before signing up for introductory offers. Avoid the pitfalls of store credit cards with tips from DCU.

How to Stretch Your Holiday Budget

Watch for these hidden holiday costs and learn how to stretch your dollar further as you shop with these tips from DCU.

How to Use Mobile Wallets for Secure Shopping

Mobile wallets are gaining in popularity as a way to make secure, contactless payments. Follow our simple tips for getting started.

Credit 101: Understanding What Credit Is and How it Works

Explore DCU's Credit 101 guide to learn the fundamentals of credit, empowering you to build your score and gain buying power.

Is Buy Now, Pay Later a Good Idea?

Interested in buy now, pay later versus using credit cards? DCU offers this resource to help detail the differences and benefits of each purchase option.

Build Your Credit with Credit Cards

Building your credit and improving your score shouldn’t be complicated. Utilizing a Visa Credit Card from DCU can help you achieve your credit goals.

Credit Cards for Everyday Spending

When and why should you use credit cards? And how can you use credit cards responsibly? DCU offers guidelines for credit card use.

Credit Cards: A Beginner’s Guide

New to credit cards? DCU helps explain the basics of credit cards — how to qualify, build credit, and spend responsibly.

How Does a Balance Transfer Affect Your Credit Score?

A balance transfer can help or hurt your credit score depending on a few factors. Learn how balance transfers work with this article from DCU.

Using Your Credit Card Wisely

Responsible use of credit cards can help you improve your credit score and make the most of your credit card rewards. Try these tips from DCU to use your credit card wisely.

Home Equity

Navigating HELOC’s: Pros, Cons, and Crucial Insights

Find out if HELOCs are a good idea for you. Read about how a HELOC can help if used correctly and what the risks are. Learn more about borrowing with DCU.

Home Renovation Money-Saving Tips

Explore tips from DCU about saving for a home renovation — including establishing and maintaining a budget, finding a contractor and financing options.

5 Smart Uses for a HELOC

A home equity line of credit (HELOC) can be a great way to fund a number of life events and financial situations. Learn how to use a HELOC to your advantage!

HELOC or Home Equity Loan: What’s the Difference?

HELOCs and Home Equity Loans both provide an opportunity to access your home’s equity with DCU. But there are a few key differences that are worth exploring.

Home Improvements With the Highest ROI

Thinking of using your HELOC for some home improvement projects? Use these ideas from DCU as a guide to help you get the most bang for your buck.

Using Your HELOC for Energy Efficient Upgrades

Energy efficiency upgrades are a great way to use your HELOC and increase the value of your home. Consider some of these green (and highly desired) updates.

When Not to Use a HELOC

Using a home equity line of credit (HELOC) is often a convenient tool, but there are times when it should be avoided. Discover how to use your HELOC wisely.

Pay Off Seasonal Spending

Seasonal spending on high interest credit cards can get expensive fast. Your HELOC can consolidate seasonal expenses and may lower your credit utilization.

How Does HELOC Utilization Affect Your Credit?

While your HELOC utilization can be reported to the credit bureaus, you can maintain or even increase your score by making timely payments.

Home Mortgage Loans

6 Tips On How to Save For Your First Home

There are many resources available to first-time home buyers. From grants to savings accounts, saving for a first home is possible, especially with the help of DCU

Fixed Rate Mortgage vs. ARM (Adjustable Rate Mortgage)

DCU examines fixed-rate versus adjustable rate mortgages, comparing and contrasting how they can serve the needs of different homebuyers.

How Much Home Can You Afford?

Buying a home may be one of the most expensive purchases you’ll make so it’s important to carefully consider your budget before setting out on the search for your dream home. You’ll want to have enough leeway so you can cover unexpected expenses, save for the future, and live the life you want.

Buyer’s Market vs. Seller’s Market: What’s the Difference?

In the world of real estate, the phrases ‘buyer’s market’ and ‘seller’s market’ can either excite you or make you apprehensive. But what exactly do they mean to you as a homebuyer or seller? This guide could help.

Homebuyer Beware: 7 Things to Watch Out For

If you’re in the market for a house, you probably have an idea of what you’re looking for. But there are also things you should make sure aren’t at your future home. Here are eight things to look out for.

What Is a Mortgage Modification, and When Would You Need One?

If you start struggling with your monthly mortgage payments, you might start worrying about what this could mean. Lenders offer a service known as mortgage modification that can provide relief and help you avoid foreclosure.

Is It a Good Time to Buy a Home?

Are you thinking of buying a home? Consider housing market trends and your own financial situation before making leap into homeownership with DCU.

Should I Rent or Buy?

Owning a home is a big part of what many consider to be the American dream. But is it always the best financial decision?

Simple Ways to Reduce Home Costs

Maintaining a home comes with plenty of rewards, but also plenty of bills, from electricity to upkeep to gas for the lawnmower. Following these seven easy tips can help you save some money along the way.

Getting Your Home Ready to Sell?

Putting your home on the market? You’ll want your home to stand out – in a good way! Consider if your home could benefit from a few updates before you place the For Sale sign out front. These tips can help you focus on what buyers will see and remember.

How Much Do I Need for Closing Costs?

If you’re preparing to buy a home, you probably have a plan in place for covering the down payment. But have you considered how to pay for closing costs? Closing costs are the expenses and fees required to complete a real estate transaction and finalize a mortgage.

When Can You Lock in a Mortgage Rate?

Searching to buy a new home and wondering if and when you can lock in a mortgage rate? Explore this guide from DCU.

Preapproval vs. prequalification – which mortgage option is right for you?

House hunting or ready to make an offer? Be prepared for any scenario by having a mortgage prequalification or a mortgage preapproval.

Buying a Home? Improve Your Credit Score First.

Focus on improving your credit and getting into great financial shape with tips from DCU before applying for a mortgage.

How Important Are Mortgage Rates?

There’s always buzz around interest rates and how they affect mortgage payments. DCU provides a customized quote and guides you through the impact mortgage rates have on your loan.

How to Make a Competitive Offer in a Seller’s Market

Are you ready to make an offer on a home in today’s competitive market? With insights from DCU, you can create a strong offer to stand out from the crowd.

Your Debt-to-Income Ratio and Why It Matters

Understanding the impact of your debt-to-income ratio and how to calculate it will help you set a budget for buying a home.

Items Needed to Apply for a Mortgage

Applying for a mortgage doesn’t have to be overwhelming if you know what to expect. Check out our mortgage application checklist and see what you may need to provide with your application.

Mortgage Refinance

Why Refinance with A Credit Union?

Refinancing your home mortgage with a credit union offers some unique advantages. Find out why refinancing with a credit union like DCU could be a smart move.

Refinancing a Mortgage: How It Works

Are you thinking about refinancing your current mortgage? DCU explains what’s involved, including the pros and cons of refinancing, and how much it can cost you.

Mortgage Refinancing 101: When is Refinancing Worth It?

Interested in paying off your mortgage faster or using better credit? Learn how refinancing your mortgage could benefit you.

What is a Cash-Out Refinance?

The equity in your home can be leveraged into cash through a cash-out refinance. DCU explains how cash-out refinancing works and when it makes financial sense.

Personal Loans

Top 10 Questions About Personal Loans

Personal loans can be used for just about anything - but how exactly do they work? DCU offers answers to 10 of the most common questions around personal loans.

How to Get a Personal Loan

Interested in taking out a personal loan, but not sure where to start? In this article we outline the process: what information you'll need, how your application is reviewed, and when you can expect the funds if approved.

Credit Cards vs. Personal Loans: What’s Right for You?

Sometimes you need to borrow money to ride out a financial emergency. To get the flexible financing you need, you may look to credit cards and personal loans to help. But how do you know which one is right for you and your needs?

When Is a Personal Loan a Good Idea?

Sometimes you need to borrow money to ride out a financial emergency. To get the flexible financing you need, you may look to credit cards and personal loans to help. But how do you know which one is right for you and your needs?

Student Loans

How to Reduce Student Loan Debt

Read tips for reducing student loan debt, including knowing your repayment plan options and making the most of your tax benefits. Learn how DCU can help.

Federal Student Loan Updates – Repayment and Next Steps

On June 30, 2023, the U.S. Supreme Court struck down the proposed federal student loan debt forgiveness program. So what happens now?

What Types of Student Loans are There?

Figuring out where to go to school is part of the puzzle, but what about student loans? DCU offers this guide that breaks down the different loan types.

Fixed vs. Variable Rate Student Loans

Discover the pros and cons of fixed and variable rate student loans, and see why borrowing from DCU is a great option for private student loans.

Ways to Pay for College-How to Fill the Funding Gap

You may know that college is your future plans, but the financial aspects of that journey may be less certain. Explore some of your college budgeting options.

How to Reduce Student Loan Payments in Times of Crisis

In times of crisis, many people have problems paying their expenses, including their monthly student loan payments. So, what are your options if you need help?

Is it Easy to Refinance Student Loans? Refinance in 5 Steps

Student loan refinance may seem complicated. DCU simplifies the process with five steps to help you determine whether you should refinance your student loans.

Why Refi Your Student Loans with a Credit Union?

You’ve decided to refinance one or more of your student loans – now how do you find the right lender? With so many options available, finding the right option can seem overwhelming. While there are many factors to consider, here are several reasons to select a credit union for your student loan refinance needs.

Budgeting/Saving

How to Start Saving for Travel

If you are preparing for a big vacation but aren’t sure how to pay for it, follow these tips from DCU to learn how to start saving for your upcoming travel.

How to Budget for Unexpected Expenses

Learn how to prepare for unexpected expenses by budgeting and saving. DCU helps members prepare for whatever the future may bring. Become a member today.

Gen Z Banking Habits

Discover how Gen Z is reshaping money habits—learn smart strategies for saving, banking, budgeting, and building credit with DCU.

How to Create a Back-to-School Budget

Learn how to navigate the expenses of back-to-school season in three easy steps, from making a list of supplies to researching costs to creating a budget.

8 Reasons Why Your Kids Need the Greenlight App

Discover 8 reasons why the Greenlight app is the perfect tool for DCU kids and families, from earning allowance to mastering financial literacy

How to Teach Your Child Financial Literacy

Did you know kids start to learn financial habits from an early age? Explore how you can teach financial literacy to your child or teen with DCU.

7 Budget-Friendly Winter Activities

No matter how you feel about winter, we all need activities to get us through the coldest season. Learn about 7 activities you can do for little or no money.

How to Reduce Your Monthly Expenses with 5 Simple Strategies

Learn how you can reduce your monthly expenses and get some breathing room in your budget with tips and advice from DCU.

Benefits of Automatic Deposits Into Savings

Discover the benefits of saving automatically and make your money work for you. Learn more about setting up automatic deposits for your savings account!

Smart Ways to Save for a New Business

Learn strategic steps for saving money to start a business. Small businesses and entrepreneurs partner with DCU. It’s easy to see why when you become a member.

Tips For Planning Your Holiday Budget

There’s no need to be a Scrooge during the holidays — DCU has the tips you need to budget responsibly while enjoying the season.

Fall Financial Cleanse: 10 Tips for Realigning Your Budget

Follow these 10 tips from DCU, a not-for-profit credit union, for saving in the fall to help set yourself up for year-end and long-term financial success.

Smart Back-to-School Money Saving Tips for Parents

The end-of-summer rush is stressful enough without having to worry about your finances. Stay smart with these back-to-school saving tips from DCU.

Tips for Budgeting and Saving on a Single Income

Read how DCU’s budgeting tips can help you and your family transition to a single income household and still save for retirement, education and more.

Weighing the Pros and Cons of a Career Break

Considering a sabbatical or career break? Weigh the following options, including the financial needs and repercussions of each choice.

How to Plan for Retirement as a Freelancer

Saving for retirement as a freelancer doesn’t have to be complicated. Find out about retirement savings account options and learn freelancer saving strategies.

How to Manage Money as a Couple

Find out helpful tips and tricks about managing finances as a couple, learning about different money personalities and how to come together to set goals.

How to Save for a Dream Vacation

Learn how much to save for a dream vacation and how budgeting can make travel affordable. Plan ahead - your dream destination doesn't have to leave you in debt.

How to Manage Finances as a Freelancer

Money management for freelancers is different from getting a salary, but it's not too complicated. Consider DCU membership for more financial education and support.

The Financial Importance of Having a Will and Estate Plan

What is a will? Who needs one? Turns out it's important for all adults to have a will. Learn the basics of estate planning when you read this article from DCU!

How To Negotiate Your Salary and Benefits

Learn about negotiating benefits and salaries to maximize your job offer, raise or promotion.

7 of the Best Ways to Use Your Tax Refund

Explore DCU’s tips on some of the best ways you can use your tax refund to save for the future and improve your financial health.

9 Common Financial Mistakes and How to Avoid Them

Learn how to avoid money problems and how planning for the unexpected can help build wealth. Let DCU help you build a healthy financial future!

Interest Rates and Annual Percentage Rate (APR) Explained

Understand how APR and interest rates differ, how both are relevant in different situations and how APR and interest rates affect your finances.

10 Benefits of Joining a Credit Union

Learn about the benefits of a credit union membership. From better interest rates to community advocacy, there are many reasons to become a member today!

What Is a High-Yield Savings Account and How Does it Work?

How do high-yield savings accounts work, exactly? Learn how your funds could be accessible while still earning you returns! Get your account started today!

How to Budget for a Wedding

Learn how much the average wedding costs, breaking down different expenses such as the venue, catering, music and more to see where you can trim your budget.

How to Avoid Overspending During the Holidays

Learn how to save for the season and prevent overspending during the holidays. Start your new year on the right financial track with help from DCU.

How to Set Financial Goals and Achieve Them

Learn why it is important to set financial goals and how to get started. With many ways to help you achieve your goals, DCU can help you take your next steps!

Are Credit Unions Safe For Your Savings?

The answer to “Are credit unions safe?” is a resounding “Yes.” Why? Learn how credit unions are protecting their members, here. Start saving with DCU, today!

How to Open a Bank Account

Learn about how opening a bank account can benefit you, and what sort of documentation you'll need to get the process started.

Why You Shouldn’t Keep Balances on Payment Apps

With the rising popularity of payment apps, it’s becoming more common to leave balances on Venmo, Cash App, and PayPal. Learn why this isn't a good idea.

How to Manage Elderly Parents' Finances

Sandwich Generation members face challenges, especially when it comes to how to manage elderly parents’ finances. Learn more with this guide from DCU.

Planning Finances & Savings for Your New Baby Arrival

Raising children is expensive and there’s a lot to figure out. DCU offers this guide to help parents with planning finances for a new baby’s arrival.

Using My Credit Card Overseas: 7 International Travel Credit Card Tips

Follow these simple tips from DCU, a not-for-profit credit union, that detail using your credit card overseas, and how you can save yourself a lot of money.

How to Get a Credit Line Increase

Learn how to get a credit line increase and whether that’s a good idea from DCU, a credit union with 23 branch locations and more than a million members.

The Importance of Emergency Funds and How To Build One

Learn how to build an emergency fund and why it’s important to have one. DCU is always here to provide financial education. Look into DCU membership today.

High-Yield Checking vs. High-Yield Savings

Your money should work hard for you, but does that mean placing it in a high-yield checking or high-yield savings account? DCU offers insight to help you understand your options.

The Secret to Saving: Track Your Spending

Learn how to make saving a priority and save money toward financial goals. DCU offers effective tips on reducing spending in order to boost savings.

Digital Tools and Tips to Simplify Saving

It’s easy for bills to pile up. Stay on track and increase your savings by using these digital tools and tips from DCU to simplify saving.

Save Money, Spend Time Enjoying Summer

We want you to make the most of the season while also reaching your financial goals, so we’ve gathered some financial tools and budget-friendly activities to help.

The Credit Union Advantage

Credit unions offer the same financial services that banks do, but typically come with several key distinctions that can make a huge difference for members.

“Extra” Paycheck? Here’s What To Do With It

Have you ever heard of an extra paycheck month? DCU explains these months when you may receive an additional paycheck and provides tips for spending and saving.

4 Smart Steps to Manage Subscription Spending

Trying to save some extra money? Consider reviewing how much you spend on subscription services in order to cut some unnecessary spending out of your monthly budget.

5 Hidden Account Fees and How to Avoid Them

Are you getting nickel and dimed by your checking account? Check out 5 hidden fees you might not realize you're paying–-and how to avoid them.

Earn More with Your Checking Account

Are you making the most of your checking account? Understanding how your checking account works and maximizing the benefits can help you reach your financial goals faster.

College Planning

How to Save For Your Child’s Education

Saving for your kids’ education is vital, and with these tips, it will become easier. Learn how to save for your child’s education with this guide.

Appealing your Award Letter

Check out this guide from DCU if you need to appeal your award package after completing your FAFSA, and have gotten your college award letter.

Do’s and Don'ts of Student Loans

It’s important to look at as many sides as possible before taking on new debt so that you can make the best decision for yourself and your future. Let’s go over some tips for you to consider as a student.

College Planning During Uncertain Times

Looking for helpful college planning resources? DCU offers these tips, which are meant to help organize you — even during uncertain times.

Do I Have To Pay Back Financial Aid

Making sense of financial aid can be confusing since there are so many different types of aid as well as parameters surrounding each type. Depending upon the type and source of financial aid, you may actually have to pay it back. Here are the different types of aid to help you better understand if and when it would need to be paid back

Additional Resources

We believe that achieving your financial goals starts with education. That’s why we’re committed to providing up-to-date, educational articles, videos, and more on our website. Additionally, all members get access to a variety of resources through our trusted partners.

Mortgage Learning Center

Purchasing a home, or refinancing, is one of life’s biggest financial decisions. Check out our new educational hub, so you can start your mortgage journey with expert knowledge.

Student Loans

Explore your loan options with our partner Credit Union Student Choice. They’ll help answer any questions you may have about the process while providing educational content on a variety of topics.

Balance Program

A free service by phone or online to provide members with confidential, no-cost financial counseling and education services.

*Membership Required. Digital Federal Credit Union members are eligible for the greenlight SELECT plan at no cost when they connect their Digital Federal Credit Union account as the Greenlight funding source for the entirety of the promotion. Subject to minimum balance requirements and identity verification. Upgrades will result in additional fees. Upon termination of promotion, members will be responsible for associated monthly fees. See terms for details. Offer ends 11/12/2026. Offer subject to change and partner participation.

853 Donald Lynch Boulevard

PO Box 9130

Marlborough, MA 01752-9130

ABA Routing Number: 211391825

NMLS# 466914

Download Our App

Federally insured by NCUA